- Tough to get accurate information | for instance, this property is for sale at $389,900. The listing states it’s got a septic system and the taxes are shown at $2,482. Curiously, the county property listing for the property shows it’s hooked-up to a Public Sewer System.

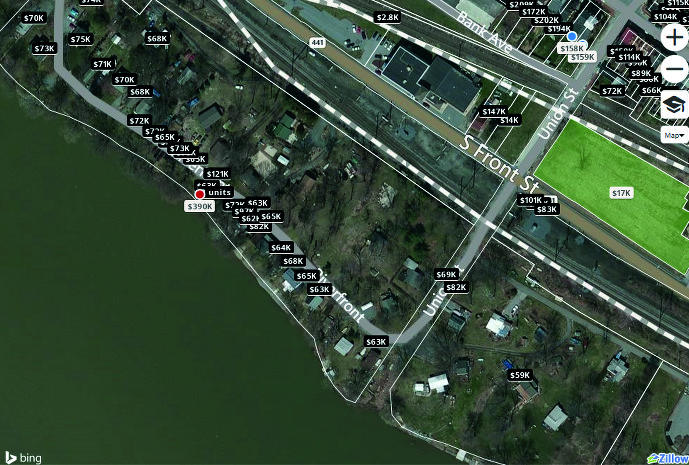

the most expensive property in the neighborhood.

the most expensive property in the neighborhood.

- Another property at 122 N 4th St, Columbia, PA 17512 is listed at zillow.com for sale for $119,900 and the taxes for that property are listed as $3,738. So the taxes are 50% higher than the property that’s for sale at over three times the price in the same town. How does that work?

- Valuation of Property – Pennsylvania assessment laws require that real estate be valued according to its “actual value” and at a bona fide rate and price for which the property would separately sell. The courts have interpreted actual value to mean market value. Market value has been defined by the Pennsylvania State Supreme Court as “the price in a competitive market a purchaser, willing but not obligated to buy, would pay an owner,willing but not obligated to sell, taking into consideration all the legal uses to which the property can be adapted and might reasonably be applied.” To establish the “actual” value of property, the county may use current year market values or it may adopt a base year for market values. For the most part, properties are assessed at a set percentage of base year values. Property is only assessed at current market value when a countywide reassessment has been conducted and implemented. Unless a county reassesses all properties every year, the property assessments will be predicated upon base year values (the last year in which the county reassessed). The same methodology must be used to value property throughout the county; that is, when a county adopts a base year for market value, then all property in the county must be valued as of the same base year. The assessment laws state that “the price at which any property may actually have been sold in the base year or the current tax year is to be considered but is not controlling. Such selling prices can be increased or decreased as part of the valuation process to accomplish equalization with other similar property within the taxing district.” Recent sales of comparable properties, that is, properties of a similar nature, are persuasive but not conclusive in helping to establish the market value. The properties selected need not be identical. The sales prices, however, are useful in showing relative values by bringing out characteristic qualities, whether similar or divergent.Comparison based on sales may be made according to location, age, income, expense, use, size, type of construction and in numerous other ways. When valuing property, three approaches must be considered in conjunction with one another; they are cost (reproduction or replacement, as applicable, less depreciation and all forms of obsolescence), comparable sales, and income approaches. Although all three approaches must be considered, they do not all have to be used in arriving at the final valuation of the property. The approach used may differ depending upon the type of property involved (e.g., commercial, residential, income-producing). – lowtaxrate.com

I believe you are missing a component to the reassment process. THIS property applied for a permit (after being reported to codes by a council woman for not having applied for a permit for the work) and once improvements are made, the permit is to be forwarded to the county reassessment office, who then comes out to review those improvements and reassess the property.

This particular property IS in fact the primary and only residential property this family owns and should not receive a 50% reduction as a second home not lived in 365 days a year, as that is exactly what it is used for.

I’m not sure that the ” 50%” reduction is entirely correct. I think the second homes are viewed as lived in half of the year or 50% of the year. That translates to a lower assessed value. With additions and upgrades, value will of course be added. Permits will reflect the improvements being made. If residents occupy the cottage year round, it can no longer be assessed as a second home.

That is correct. All permits end up at the Lancaster County Tax Assessment Office for review and they play a part in the reassessment process. That is why everyone must apply for a permit, otherwise those that do are paying the price for those that cheat and do not get one. Recently the tax assessment office reported that there are 165 permits out in Columbia. The cottages are not exempt from requiring the purchase of a permit.

Appreciate your comment, but we are wondering about the disparate tax for two properties with a wide gap in asking price. And wondering how the property got listed with PUBLIC SEWER. We’re unaware of a public sewer line in that area. Is there one?

The MLS listing states the property has septic not public sewer.

Yep, it does! As does the sale listing. But the County property ownership site says “public sewer.”

http://lcapp1.co.lancaster.pa.us/aoweb/ParcelDetails.aspx?ParcelID=1107295610017|&searchType=propAdd&streetnum=&streetDir=&streetName=river%20front&streetSuffix=

One point of the observation is that it’s tough to get information that is reliable.

There is no public sewer currently available on the street / road known as River Front.